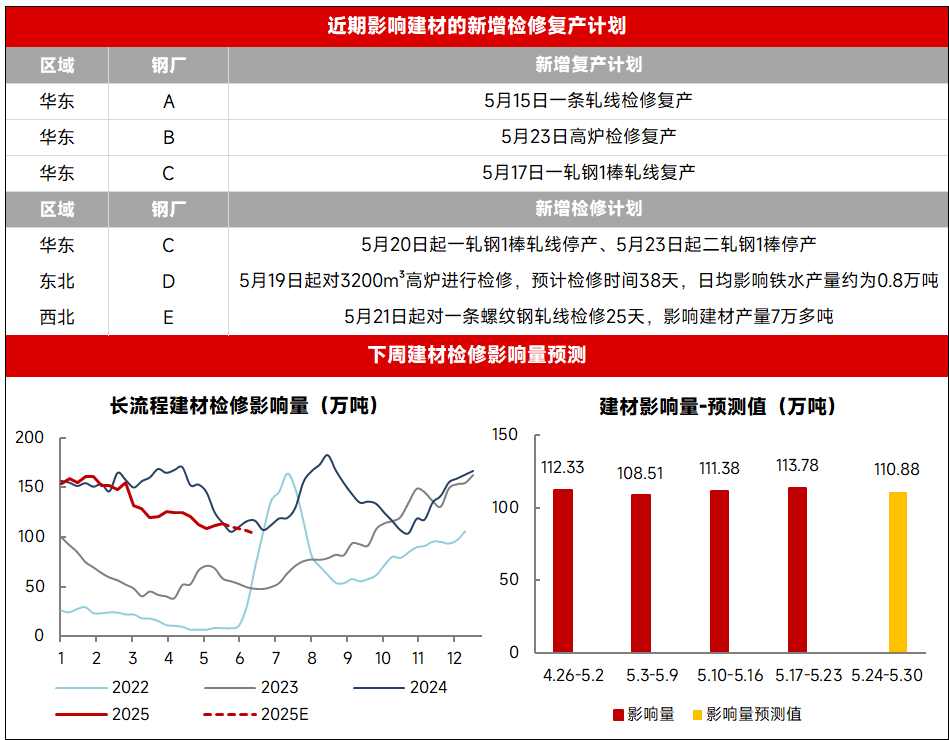

According to the SMM survey, the impact of maintenance on construction materials continued to increase slightly this week (5.17-5.23). Some steel mills' blast furnaces and rebar rolling lines began maintenance as scheduled this week, with the impact of maintenance on construction materials reaching 1.1378 million mt, an increase of 24,000 mt WoW.

Source: SMM

Stimulated by the news of the implementation of tariff reductions in Sino-US trade, prices of raw materials and finished steel products increased to varying degrees last week. Currently, blast furnace pig iron production remains at a high level, providing strong demand support for raw materials such as iron ore and coke. However, the end-use demand for finished steel products is gradually weakening, leading to an overall slightly stronger performance of raw materials compared to finished steel products. The production profit margin for rebar has narrowed slightly, but steel mills still maintain a profit of around 100 yuan per mt, and their production enthusiasm remains strong. According to the SMM survey, a steel mill in the north-west China region postponed the start of maintenance on its rebar rolling line, while a steel mill in the south-west China region completed blast furnace maintenance and resumed production. However, considering that steel mills' blast furnaces and rolling lines in the north-east China and east China regions are still undergoing scheduled maintenance this week, the impact of maintenance on construction materials has increased slightly this week.

Looking ahead, as the buzz around the Sino-US trade news gradually fades this week, the market is returning to fundamentals. The latest data shows that various operational indicators in the end-use real estate sector are in a downturn. Coupled with the increase in rainy weather in south China, which has affected construction progress, the overall demand resilience for construction materials is insufficient, and the market sentiment is cautious. It is expected that spot market prices will come under pressure this week, but currently, producers have a strong willingness to refuse to budge on prices, so the downside room for prices is limited. The extent of the short-term reduction in rebar profits will remain within a mild range, and steel mills' production enthusiasm is unlikely to diminish. Next week, some steel mills are still expected to resume production as scheduled. It is estimated that the impact of maintenance on construction materials will be 1.1088 million mt next week, a decrease of 29,000 mt WoW.

Source: SMM

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)